Table of Contents

ToggleIntroduction–

Financial education for children is an essential aspect of preparing the next generation for success in an increasingly complex and dynamic world. In today’s society, where financial decisions play a significant role in shaping individuals’ lives, instilling financial literacy from a young age is more important than ever. By providing children with the knowledge, skills, and attitudes necessary to manage money effectively, financial education sets the foundation for lifelong financial well-being and success.

In this introduction, we will explore the importance of financial education for children, the key concepts and skills it encompasses, and the benefits it offers to young learners. From budgeting and saving to investing and responsible spending, financial education equips children with the tools they need to make informed financial decisions, navigate financial challenges, and achieve their financial goals. Let’s delve into the world of financial education for children and discover why it’s an essential aspect of their development and future success.

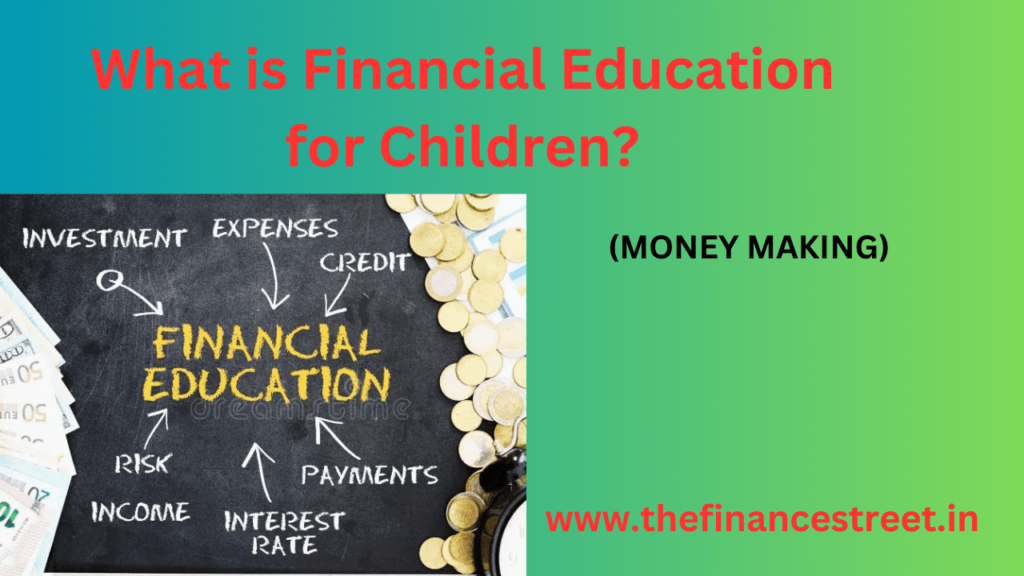

What is Financial Education for Children?

Financial education for children involves teaching young individuals about money management, budgeting, saving, investing, and other aspects of personal finance. The goal is to instill in children a strong foundation of financial literacy and skills that will empower them to make informed decisions about money as they grow older. Here are some key components of financial education for children:

- Basic Money Concepts: Introducing children to fundamental concepts such as earning, spending, saving, and sharing. This includes teaching them about different forms of currency, like coins and bills, and their respective values.

- Budgeting Skills: Teaching children how to create and stick to a budget by allocating money for different purposes, such as savings, spending, and giving. This helps them understand the importance of prioritizing their expenses and making wise financial choices.

- Saving and Goal Setting: Encouraging children to develop a habit of saving money for short-term and long-term goals. This could involve setting up a savings account for them and helping them track their progress toward achieving their financial goals.

- Understanding Needs vs. Wants: Helping children distinguish between essential needs and discretionary wants. Teaching them to prioritize spending on necessities while being mindful of impulse purchases can instill good financial habits early on.

- Introduction to Banking: Introducing children to the basic functions of banks, such as depositing money, withdrawing funds, and understanding interest. Teaching them about the role of banks in safeguarding their money can help them become more comfortable with financial institutions.

- Consumer Awareness: Educating children about consumerism and advertising, teaching them to be critical consumers who evaluate products and make informed purchasing decisions based on value and quality rather than marketing hype.

- Introduction to Investing: Introducing children to the concept of investing and explaining the potential benefits of investing for the future. This could include discussing simple investment vehicles like stocks, bonds, and mutual funds in age-appropriate terms.

- Risk Management: Teaching children about the concept of risk and reward in financial decision-making. This involves helping them understand the potential risks associated with different financial choices and the importance of making informed decisions to mitigate those risks.

- Charitable Giving: Encouraging children to develop a sense of social responsibility by teaching them about the importance of giving back to their community through charitable donations or volunteering.

Overall, financial education for children aims to equip them with the knowledge, skills, and attitudes necessary to become financially responsible adults who can effectively manage their money and achieve their financial goals.

Why is Financial Education important for Children?

Financial education is crucial for children for several reasons:

- Early Financial Habits: Teaching children about money management from a young age helps them develop healthy financial habits early on. By instilling concepts like budgeting, saving, and responsible spending during childhood, they are more likely to carry these habits into adulthood.

- Empowerment: Financial education empowers children to make informed decisions about money. It equips them with the knowledge and skills to navigate financial challenges and opportunities confidently, enabling them to take control of their financial futures.

- Critical Life Skill: Understanding how to manage money is a critical life skill that children need to succeed in adulthood. Financial literacy is essential for everyday tasks such as budgeting, paying bills, and saving for goals, as well as making larger financial decisions like buying a home or investing for retirement.

- Preventing Debt and Financial Struggles: Without a solid understanding of financial principles, children may be more susceptible to debt and financial struggles later in life. Financial education helps them develop the discipline to live within their means, avoid unnecessary debt, and plan for unexpected expenses.

- Building Wealth: Financially literate children are better positioned to build wealth over time. By learning about concepts like investing and compound interest, they can leverage their knowledge to grow their savings and investments, setting themselves up for financial success in the long run.

- Consumer Protection: With the rise of digital transactions and online shopping, children need to understand how to protect themselves from financial scams and fraud. Financial education teaches them to recognize potential risks and make safe and responsible financial choices.

- Fostering Independence: Teaching children about financial responsibility fosters independence and self-reliance. As they learn to manage their money effectively, they gain a sense of autonomy and confidence in their ability to handle financial matters on their own.

- Social and Economic Participation: Financially literate individuals are better positioned to participate fully in society and the economy. They are more likely to secure stable employment, contribute to economic growth, and make informed decisions as consumers and investors.

Overall, financial education lays the foundation for children to build a secure financial future and achieve their goals. By investing in their financial literacy early on, we empower them to lead financially healthy and fulfilling lives.

How do you teach Children about finances?

Teaching children about finances can be done through various methods and approaches tailored to their age and developmental stage. Here are some effective ways to teach children about finances:

- Start Early: Introduce basic money concepts to children as early as preschool age. Use simple activities like counting coins, playing store, or setting up a pretend bank to teach them about the value of money.

- Use Everyday Examples: Incorporate financial lessons into everyday experiences. For example, involve children in grocery shopping and budgeting decisions, or discuss the cost of items they want to buy and encourage them to compare prices.

- Lead by Example: Children learn by observing and imitating adults. Model good financial habits and behaviors, such as budgeting, saving, and avoiding impulse purchases. Explain your financial decisions and involve children in family financial discussions when appropriate.

- Make it Fun and Interactive: Use games, puzzles, and interactive activities to make learning about finances enjoyable for children. There are many board games, online apps, and educational resources designed specifically to teach financial concepts in a fun and engaging way.

- Set Allowance and Savings Goals: Give children an allowance or opportunities to earn money through chores or tasks. Encourage them to allocate a portion of their earnings to savings goals and discuss the importance of saving for short-term and long-term objectives.

- Teach Budgeting Skills: Help children create a simple budget by dividing their money into categories such as saving, spending, and giving. Encourage them to track their expenses and adjust their budget as needed to meet their financial goals.

- Explore Financial Literacy Books and Resources: There are many children’s books, videos, and online resources available that teach financial concepts in a way that is easy for kids to understand. Use these resources to reinforce lessons and spark discussions about money.

- Encourage Critical Thinking: Teach children to be critical consumers by discussing advertising techniques, comparing prices and features of products, and considering the value of purchases before making decisions.

- Introduce Banking Concepts: Take children to the bank to open a savings account in their name. Explain how banks work, including concepts like deposits, withdrawals, interest, and the importance of keeping money safe.

- Discuss Real-life Financial Scenarios: As children get older, engage them in discussions about real-life financial scenarios, such as saving for college, planning for big purchases, or dealing with unexpected expenses. Encourage them to brainstorm solutions and make decisions based on financial principles they have learned.

By incorporating these strategies into everyday interactions and activities, parents, educators, and caregivers can help children develop a strong foundation of financial literacy that will serve them well throughout their lives.

What are the benefits of early Financial education to Children?

Early financial education offers numerous benefits to children:

- Developing Financial Literacy: Early exposure to financial concepts helps children develop a solid understanding of money management, budgeting, saving, investing, and other financial skills. This knowledge lays the foundation for making informed financial decisions later in life.

- Building Responsible Financial Habits: By learning about money at a young age, children are more likely to develop responsible financial habits and behaviors. They learn the importance of saving, budgeting, and making wise spending choices, which can set them up for financial success in adulthood.

- Empowering Financial Independence: Financially literate children gain a sense of empowerment and independence in managing their money. They feel confident making financial decisions and are better equipped to navigate financial challenges as they grow older.

- Fostering Critical Thinking Skills: Learning about finances encourages children to think critically and analytically about money-related issues. They learn to evaluate financial choices, weigh risks and rewards, and make informed decisions based on their understanding of financial principles.

- Preparing for Future Financial Challenges: Early financial education equips children with the skills and knowledge they need to navigate the complex financial landscape they will encounter as adults. They learn how to save for goals, manage debt, plan for emergencies, and invest for the future, preparing them to handle various financial challenges with confidence.

- Reducing Financial Stress: Financially literate children are less likely to experience financial stress and anxiety as adults. By learning how to manage their money effectively from a young age, they develop the skills and confidence to handle financial setbacks and unexpected expenses without feeling overwhelmed.

- Promoting Financial Responsibility: Early financial education instills a sense of responsibility and accountability in children regarding their financial choices. They learn to take ownership of their financial decisions and understand the consequences of their actions, which promotes responsible money management behavior.

- Encouraging Goal Setting and Achievement: Children who receive early financial education are more likely to set and achieve financial goals throughout their lives. Whether it’s saving for a toy, a college education, or a dream vacation, they learn the importance of setting goals, creating a plan to achieve them, and staying committed to their objectives.

Overall, early financial education provides children with essential knowledge, skills, and attitudes that contribute to their overall financial well-being and success in life. By investing in financial literacy from a young age, we empower children to build a solid financial foundation and thrive in an increasingly complex financial world.

What is the difference between Academic & Financial Education?

The difference between academic education and financial education lies in the subject matter and focus of each:

- Academic Education: Academic education typically refers to the formal schooling and learning of subjects such as mathematics, science, language arts, history, and other traditional academic disciplines. It encompasses a broad range of knowledge and skills necessary for intellectual and personal development, as well as for pursuing higher education and entering various professions.

- Financial Education: Financial education, on the other hand, focuses specifically on teaching individuals about money management, budgeting, saving, investing, and other aspects of personal finance. It aims to equip individuals with the knowledge, skills, and attitudes necessary to make informed financial decisions, achieve financial goals, and navigate the financial challenges of everyday life.

In summary, while academic education provides a broad foundation of knowledge across various subjects, financial education hones in on specific financial concepts and skills essential for managing money effectively and achieving financial well-being. Both forms of education are important for personal development and success in life, but they serve different purposes and address different aspects of learning.

Critical Analysis of Financial Education for Children in India-

Critical analysis of financial education for children in India reveals both strengths and weaknesses:

Strengths:

- Recognition of Importance: There is a growing recognition of the importance of financial education for children in India. Many educational institutions and policymakers have acknowledged the need to incorporate financial literacy into the school curriculum.

- Government Initiatives: The Government of India has launched initiatives such as the National Strategy for Financial Education (NSFE) to promote financial literacy among children and youth. These initiatives aim to raise awareness about financial concepts and empower children to make informed financial decisions.

- Curriculum Integration: Some schools have begun integrating financial education into their curriculum through dedicated subjects or modules. This helps ensure that children receive structured instruction in financial literacy from an early age.

- Public Awareness Campaigns: Various public and private organizations in India conduct financial literacy programs and awareness campaigns targeted at children and youth. These initiatives help raise awareness about financial matters and promote the importance of financial education.

Weaknesses:

- Limited Coverage: Despite efforts to promote financial education, coverage remains limited, particularly in rural and underserved areas. Many children in India still lack access to quality financial education due to factors such as inadequate resources, lack of trained educators, and competing priorities in the education system.

- Quality of Instruction: The quality of financial education provided to children in India varies widely. While some schools offer comprehensive programs, others may provide only superficial or outdated information. There is a need to ensure that educators are properly trained and equipped to teach financial concepts effectively.

- Lack of Standardization: Financial education programs in India lack standardization, leading to inconsistencies in content and delivery. There is a need for standardized guidelines and curriculum frameworks to ensure that children receive consistent and high-quality financial education across different schools and regions.

- Focus on Rote Learning: The Indian education system often prioritizes rote learning over practical application and critical thinking. As a result, children may memorize financial concepts without fully understanding their relevance or how to apply them in real-life situations.

- Socioeconomic Disparities: Socioeconomic disparities exacerbate the challenges of financial education in India. Children from low-income families may face additional barriers to accessing quality financial education, perpetuating cycles of financial illiteracy and poverty.

Overall, while there have been positive developments in promoting financial education for children in India, significant challenges remain in terms of coverage, quality, standardization, and addressing socioeconomic disparities. Addressing these challenges will require sustained efforts from policymakers, educators, parents, and other stakeholders to ensure that all children have access to the financial knowledge and skills they need to thrive in an increasingly complex financial world.

Conclusion –

In conclusion, financial education for children is a critical component of their overall development and well-being. By equipping children with the knowledge, skills, and attitudes necessary to manage money effectively, financial education sets them on a path toward financial literacy and success in adulthood.

Through early exposure to financial concepts and practical lessons in budgeting, saving, investing, and responsible spending, children learn valuable skills that will serve them throughout their lives. Financial education empowers children to make informed financial decisions, build responsible financial habits, and navigate the complexities of the modern financial landscape with confidence.

While progress has been made in promoting financial education for children, there are still challenges to address, including issues of coverage, quality, standardization, and socioeconomic disparities. However, with continued efforts from policymakers, educators, parents, and other stakeholders, we can work towards ensuring that all children have access to high-quality financial education that prepares them for a financially secure future.

In essence, investing in financial education for children is an investment in their future prosperity and well-being, providing them with the tools they need to achieve their financial goals, fulfill their potential, and contribute positively to society. By prioritizing financial education for children, we can empower the next generation to build brighter financial futures for themselves and for generations to come.